General Middleware

Creating Decision Trees for Classification Problems – Find Loan delinquency

Context

DRS bank is facing challenging times. Their NPAs (Non-Performing Assets) has been on a rise recently and a large part of these are due to the loans given to individual customers(borrowers). Chief Risk Officer of the bank decides to put in a scientifically robust framework for approval of loans to individual customers to minimize the risk of loans converting into NPAs and initiates a project for the data science team at the bank. You, as a senior member of the team, are assigned this project.

Objective

To identify the criteria to approve loans for an individual customer such that the likelihood of the loan delinquency is minimized

Key questions to be answered

What are the factors that drive the behavior of loan delinquency?

Dataset

- ID: Customer ID

- isDelinquent : indicates whether the customer is delinquent or not (1 => Yes, 0 => No)

- term: Loan term in months

- gender: Gender of the borrower

- age: Age of the borrower

- purpose: Purpose of Loan

- home_ownership: Status of borrower’s home

- FICO: FICO (i.e. the bureau score) of the borrower

Domain Information

- Transactor – A person who pays his due amount balance full and on time.

- Revolver – A person who pays the minimum due amount but keeps revolving his balance and does not pay the full amount.

- Delinquent – Delinquency means that you are behind on payments, a person who fails to pay even the minimum due amount.

- Defaulter – Once you are delinquent for a certain period your lender will declare you to be in the default stage.

- Risk Analytics – A wide domain in the financial and banking industry, basically analyzing the risk of the customer.

Import the necessary packages

In [1]:

# this will help in making the Python code more structured automatically (good coding practice)

%load_ext nb_black

# Library to suppress warnings or deprecation notes

import warnings

warnings.filterwarnings("ignore")

# Libraries to help with reading and manipulating data

import pandas as pd

import numpy as np

# Library to split data

from sklearn.model_selection import train_test_split

# libaries to help with data visualization

import matplotlib.pyplot as plt

import seaborn as sns

# Removes the limit for the number of displayed columns

pd.set_option("display.max_columns", None)

# Sets the limit for the number of displayed rows

pd.set_option("display.max_rows", 200)

# Libraries to build decision tree classifier

from sklearn.tree import DecisionTreeClassifier

from sklearn import tree

# To tune different models

from sklearn.model_selection import GridSearchCV

# To get diferent metric scores

from sklearn.metrics import (

f1_score,

accuracy_score,

recall_score,

precision_score,

confusion_matrix,

plot_confusion_matrix,

make_scorer,

)

Read the dataset

In [2]:

data = pd.read_csv("Loan_Delinquent_Dataset.csv")

In [3]:

# copying data to another varaible to avoid any changes to original data loan = data.copy()

View the first and last 5 rows of the dataset.

In [4]:

loan.head()

Out[4]:

| ID | isDelinquent | term | gender | purpose | home_ownership | age | FICO | |

|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 1 | 36 months | Female | House | Mortgage | >25 | 300-500 |

| 1 | 2 | 0 | 36 months | Female | House | Rent | 20-25 | >500 |

| 2 | 3 | 1 | 36 months | Female | House | Rent | >25 | 300-500 |

| 3 | 4 | 1 | 36 months | Female | Car | Mortgage | >25 | 300-500 |

| 4 | 5 | 1 | 36 months | Female | House | Rent | >25 | 300-500 |

In [5]:

loan.tail()

Out[5]:

| ID | isDelinquent | term | gender | purpose | home_ownership | age | FICO | |

|---|---|---|---|---|---|---|---|---|

| 11543 | 11544 | 0 | 60 months | Male | other | Mortgage | >25 | 300-500 |

| 11544 | 11545 | 1 | 36 months | Male | House | Rent | 20-25 | 300-500 |

| 11545 | 11546 | 0 | 36 months | Female | Personal | Mortgage | 20-25 | >500 |

| 11546 | 11547 | 1 | 36 months | Female | House | Rent | 20-25 | 300-500 |

| 11547 | 11548 | 1 | 36 months | Male | Personal | Mortgage | 20-25 | 300-500 |

Understand the shape of the dataset.

In [6]:

loan.shape

Out[6]:

(11548, 8)

- The dataset has 11548 rows and 8 columns of data

Check the data types of the columns for the dataset.

In [7]:

loan.info()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 11548 entries, 0 to 11547 Data columns (total 8 columns): # Column Non-Null Count Dtype --- ------ -------------- ----- 0 ID 11548 non-null int64 1 isDelinquent 11548 non-null int64 2 term 11548 non-null object 3 gender 11548 non-null object 4 purpose 11548 non-null object 5 home_ownership 11548 non-null object 6 age 11548 non-null object 7 FICO 11548 non-null object dtypes: int64(2), object(6) memory usage: 721.9+ KB

Observations –

- isDelinquent is the dependent variable – type integer.

- All the dependent variables except for ID are object type.

Summary of the dataset.

In [8]:

loan.describe(include="all")

Out[8]:

| ID | isDelinquent | term | gender | purpose | home_ownership | age | FICO | |

|---|---|---|---|---|---|---|---|---|

| count | 11548.000000 | 11548.000000 | 11548 | 11548 | 11548 | 11548 | 11548 | 11548 |

| unique | NaN | NaN | 2 | 2 | 7 | 3 | 2 | 2 |

| top | NaN | NaN | 36 months | Male | House | Mortgage | 20-25 | 300-500 |

| freq | NaN | NaN | 10589 | 6555 | 6892 | 5461 | 5888 | 6370 |

| mean | 5774.500000 | 0.668601 | NaN | NaN | NaN | NaN | NaN | NaN |

| std | 3333.764789 | 0.470737 | NaN | NaN | NaN | NaN | NaN | NaN |

| min | 1.000000 | 0.000000 | NaN | NaN | NaN | NaN | NaN | NaN |

| 25% | 2887.750000 | 0.000000 | NaN | NaN | NaN | NaN | NaN | NaN |

| 50% | 5774.500000 | 1.000000 | NaN | NaN | NaN | NaN | NaN | NaN |

| 75% | 8661.250000 | 1.000000 | NaN | NaN | NaN | NaN | NaN | NaN |

| max | 11548.000000 | 1.000000 | NaN | NaN | NaN | NaN | NaN | NaN |

Observations-

- Most of the loans are for a 36-month term loan.

- More males have applied for loans than females.

- Most loan applications are for house loans.

- Most customers have either mortgaged their houses.

- Mostly customers in the age group 20-25 have applied for a loan.

- Most customers have a FICO score between 300 and 500.

In [9]:

# checking for unique values in ID column loan["ID"].nunique()

Out[9]:

11548

- Since all the values in ID column are unique we can drop it

In [10]:

loan.drop(["ID"], axis=1, inplace=True)

Check for missing values

In [11]:

loan.isnull().sum()

Out[11]:

isDelinquent 0 term 0 gender 0 purpose 0 home_ownership 0 age 0 FICO 0 dtype: int64

- There are no missing vaues in out dataset

Univariate analysis

In [12]:

# function to create labeled barplots

def labeled_barplot(data, feature, perc=False, n=None):

"""

Barplot with percentage at the top

data: dataframe

feature: dataframe column

perc: whether to display percentages instead of count (default is False)

n: displays the top n category levels (default is None, i.e., display all levels)

"""

total = len(data[feature]) # length of the column

count = data[feature].nunique()

if n is None:

plt.figure(figsize=(count + 2, 6))

else:

plt.figure(figsize=(n + 2, 6))

plt.xticks(rotation=90, fontsize=15)

ax = sns.countplot(

data=data,

x=feature,

palette="Paired",

order=data[feature].value_counts().index[:n].sort_values(),

)

for p in ax.patches:

if perc == True:

label = "{:.1f}%".format(

100 * p.get_height() / total

) # percentage of each class of the category

else:

label = p.get_height() # count of each level of the category

x = p.get_x() + p.get_width() / 2 # width of the plot

y = p.get_height() # height of the plot

ax.annotate(

label,

(x, y),

ha="center",

va="center",

size=12,

xytext=(0, 5),

textcoords="offset points",

) # annotate the percentage

plt.show() # show the plot

Observations on isDelinquent

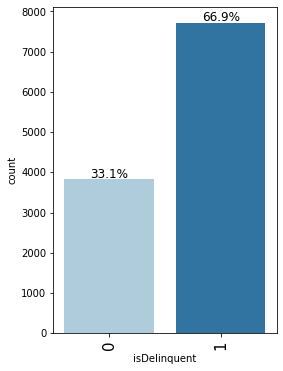

In [13]:

labeled_barplot(loan, "isDelinquent", perc=True)

- 66.9% of the customers are delinquent

Observations on term

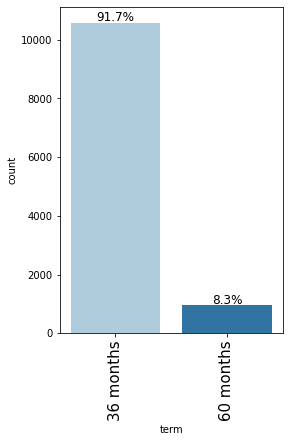

In [14]:

labeled_barplot(loan, "term", perc=True)

- 91.7% of the loans are for a 36 month term.

Observations on gender

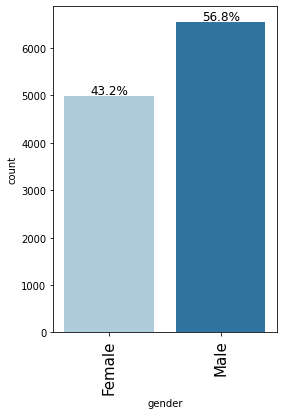

In [15]:

labeled_barplot(loan, "gender", perc=True)

- There are more male applicants (56.8%) than female applicants (43.2%)

Observations on purpose

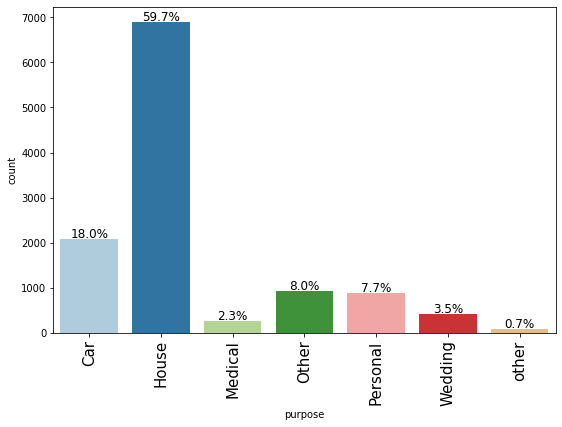

In [16]:

labeled_barplot(loan, "purpose", perc=True)

- Most loan applications are for house loans (59.7%) followed by car loans (18%)

- There are 2 levels named ‘other’ and ‘Other’ under the purpose variable. Since we do not have any other information about these, we can merge these levels.

Observations on home_ownership

In [17]:

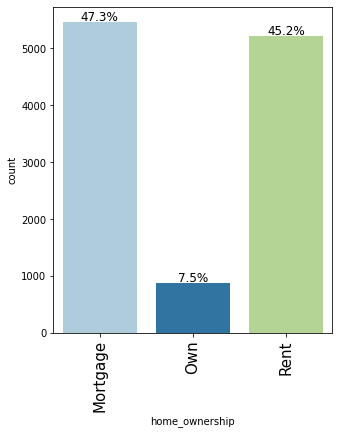

labeled_barplot(loan, "home_ownership", perc=True)

- Very few applicants <10% own their house, Most customers have either mortgaged their houses or live on rent.

Observations on age

In [18]:

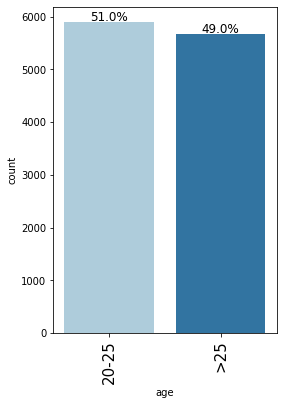

labeled_barplot(loan, "age", perc=True)

- Almost an equal percentage of people aged 20-25 and >25 have applied for the loan.

Observations on FICO

In [19]:

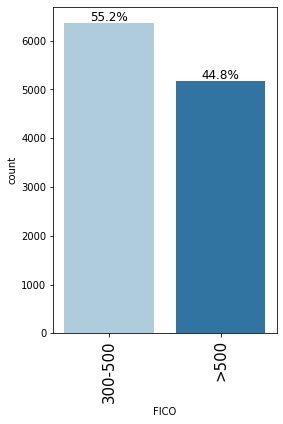

labeled_barplot(loan, "FICO", perc=True)

- Most customers have a FICO score between 300 and 500 (55.2%) followed by a score of greater than 500 (44.8%)

Data Cleaning

In [20]:

loan["purpose"].unique()

Out[20]:

array(['House', 'Car', 'Other', 'Personal', 'Wedding', 'Medical', 'other'],

dtype=object)

We can merge the purpose – ‘other’ and ‘Other’ together

In [21]:

loan["purpose"].replace("other", "Other", inplace=True)

In [22]:

loan["purpose"].unique()

Out[22]:

array(['House', 'Car', 'Other', 'Personal', 'Wedding', 'Medical'],

dtype=object)

Bivariate Analysis

In [23]:

# function to plot stacked bar chart

def stacked_barplot(data, predictor, target):

"""

Print the category counts and plot a stacked bar chart

data: dataframe

predictor: independent variable

target: target variable

"""

count = data[predictor].nunique()

sorter = data[target].value_counts().index[-1]

tab1 = pd.crosstab(data[predictor], data[target], margins=True).sort_values(

by=sorter, ascending=False

)

print(tab1)

print("-" * 120)

tab = pd.crosstab(data[predictor], data[target], normalize="index").sort_values(

by=sorter, ascending=False

)

tab.plot(kind="bar", stacked=True, figsize=(count + 5, 6))

plt.legend(

loc="lower left", frameon=False,

)

plt.legend(loc="upper left", bbox_to_anchor=(1, 1))

plt.show()

In [24]:

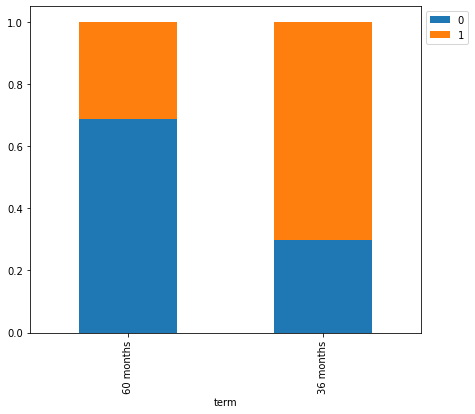

stacked_barplot(loan, "term", "isDelinquent")

isDelinquent 0 1 All term All 3827 7721 11548 36 months 3168 7421 10589 60 months 659 300 959 ------------------------------------------------------------------------------------------------------------------------

- Most loan delinquent customers have taken loan for 36 months.

In [25]:

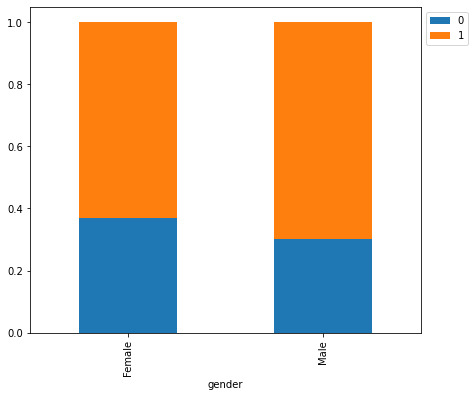

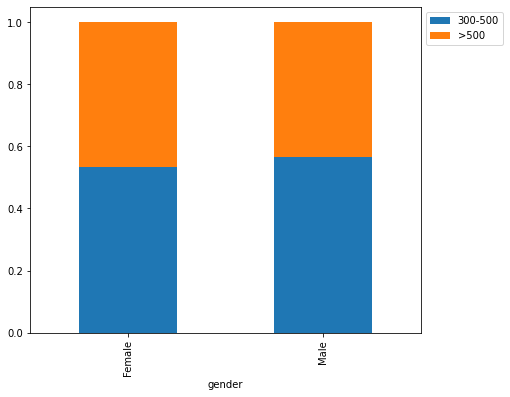

stacked_barplot(loan, "gender", "isDelinquent")

isDelinquent 0 1 All gender All 3827 7721 11548 Male 1977 4578 6555 Female 1850 3143 4993 ------------------------------------------------------------------------------------------------------------------------

- There’s not much difference between male and female customers.

In [26]:

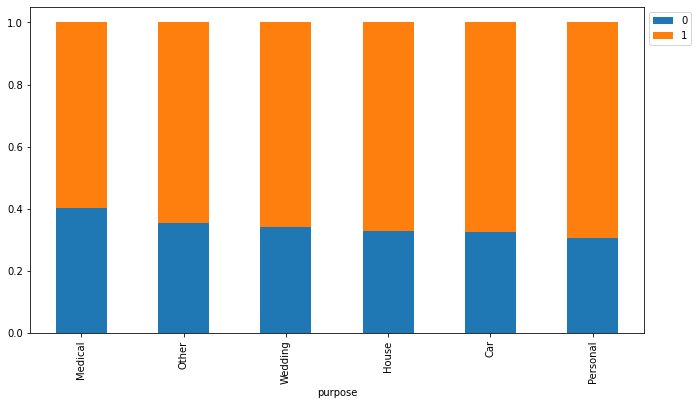

stacked_barplot(loan, "purpose", "isDelinquent")

isDelinquent 0 1 All purpose All 3827 7721 11548 House 2272 4620 6892 Car 678 1402 2080 Other 357 653 1010 Personal 274 618 892 Wedding 139 269 408 Medical 107 159 266 ------------------------------------------------------------------------------------------------------------------------

- Most loan delinquent customers are those who have applied for house loans followed by car and personal loans.

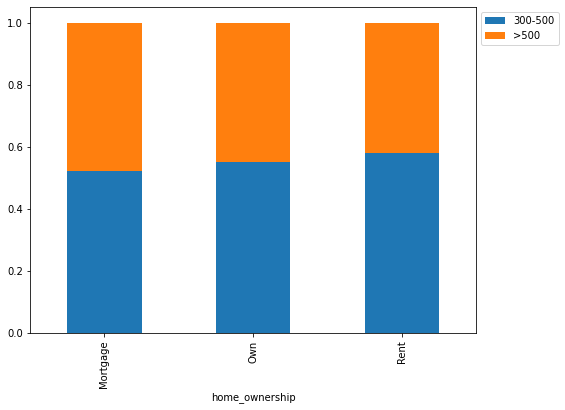

In [27]:

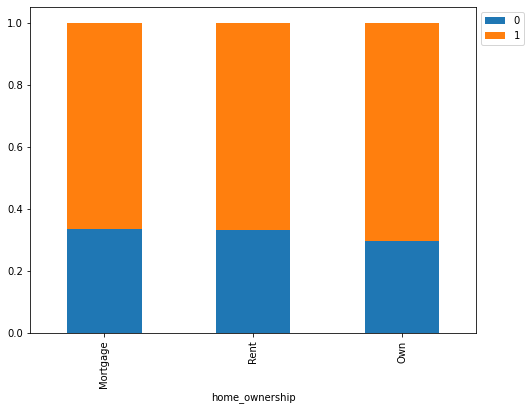

stacked_barplot(loan, "home_ownership", "isDelinquent")

isDelinquent 0 1 All home_ownership All 3827 7721 11548 Mortgage 1831 3630 5461 Rent 1737 3479 5216 Own 259 612 871 ------------------------------------------------------------------------------------------------------------------------

- Those customers who have their own house are less delinquent than the ones who live in a rented place or have mortgaged their home.

In [28]:

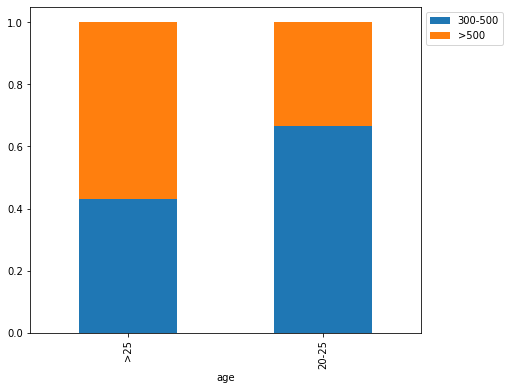

stacked_barplot(loan, "age", "isDelinquent")

isDelinquent 0 1 All age All 3827 7721 11548 >25 1969 3691 5660 20-25 1858 4030 5888 ------------------------------------------------------------------------------------------------------------------------

- Customers between 20-25 years of age are more delinquent.

In [29]:

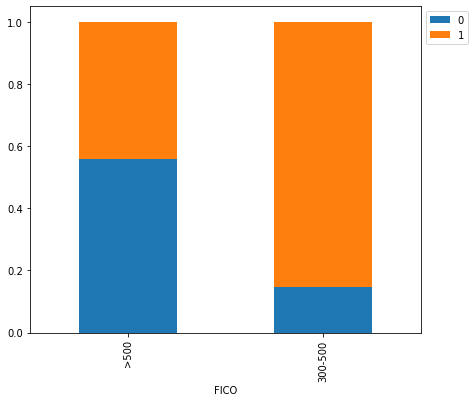

stacked_barplot(loan, "FICO", "isDelinquent")

isDelinquent 0 1 All FICO All 3827 7721 11548 >500 2886 2292 5178 300-500 941 5429 6370 ------------------------------------------------------------------------------------------------------------------------

- If FICO score is >500 the chances of delinquency decrease quite a lot compared to when FICO score is between 300-500.

Key Observations –

- FICO score and term of loan application appear to be very strong indicators of delinquency.

- Other factors appear to be not very good indicators of delinquency. (We can use chi-square tests to determine statistical significance in the association between two categorical variables).

We observed that a high FICO score means that the chances of delinquency are lower, let us see if any of the other variables indicate higher a FICO score.

In [30]:

stacked_barplot(loan, "home_ownership", "FICO")

FICO 300-500 >500 All home_ownership All 6370 5178 11548 Mortgage 2857 2604 5461 Rent 3033 2183 5216 Own 480 391 871 ------------------------------------------------------------------------------------------------------------------------

In [31]:

stacked_barplot(loan, "age", "FICO")

FICO 300-500 >500 All age All 6370 5178 11548 >25 2443 3217 5660 20-25 3927 1961 5888 ------------------------------------------------------------------------------------------------------------------------

In [32]:

stacked_barplot(loan, "gender", "FICO")

FICO 300-500 >500 All gender All 6370 5178 11548 Male 3705 2850 6555 Female 2665 2328 4993 ------------------------------------------------------------------------------------------------------------------------

Key Observations

- Home ownership and gender seem to have a slight impact on the FICO scores.

- Age seems to have a much bigger impact on FICO scores.

Model Building – Approach

- Data preparation

- Partition the data into train and test set.

- Built a CART model on the train data.

- Tune the model and prune the tree, if required.

Split Data

In [36]:

X = loan.drop(["isDelinquent"], axis=1) y = loan["isDelinquent"]

In [37]:

# encoding the categorical variables X = pd.get_dummies(X, drop_first=True) X.head()

Out[37]:

| term_60 months | gender_Male | purpose_House | purpose_Medical | purpose_Other | purpose_Personal | purpose_Wedding | home_ownership_Own | home_ownership_Rent | age_>25 | FICO_>500 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

| 1 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | 1 |

| 2 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 |

| 3 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 |

| 4 | 0 | 0 | 1 | 0 | 0 | 0 | 0 | 0 | 1 | 1 | 0 |

In [38]:

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.4, random_state=1)

In [39]:

print("Number of rows in train data =", X_train.shape[0])

print("Number of rows in test data =", X_test.shape[0])

Number of rows in train data = 6928 Number of rows in test data = 4620

In [40]:

print("Percentage of classes in training set:")

print(y_train.value_counts(normalize=True))

print("Percentage of classes in test set:")

print(y_test.value_counts(normalize=True))

Percentage of classes in training set: 1 0.677396 0 0.322604 Name: isDelinquent, dtype: float64 Percentage of classes in test set: 1 0.655411 0 0.344589 Name: isDelinquent, dtype: float64

Build Decision Tree Model

Model evaluation criterion

Model can make wrong predictions as:

- Predicting a customer will not be behind on payments (Non-Delinquent) but in reality the customer would be behind on payments.

- Predicting a customer will be behind on payments (Delinquent) but in reality the customer would not be behind on payments (Non-Delinquent).

Which case is more important?

- If we predict a non-delinquent customer as a delinquent customer bank would lose an opportunity of providing loan to a potential customer.

How to reduce this loss i.e need to reduce False Negatives?

recallshould be maximized, the greater the recall higher the chances of minimizing the false negatives.

First, let’s create functions to calculate different metrics and confusion matrix so that we don’t have to use the same code repeatedly for each model.

- The model_performance_classification_sklearn function will be used to check the model performance of models.

- The make_confusion_matrix function will be used to plot confusion matrix.

In [41]:

# defining a function to compute different metrics to check performance of a classification model built using sklearn

def model_performance_classification_sklearn(model, predictors, target):

"""

Function to compute different metrics to check classification model performance

model: classifier

predictors: independent variables

target: dependent variable

"""

# predicting using the independent variables

pred = model.predict(predictors)

acc = accuracy_score(target, pred) # to compute Accuracy

recall = recall_score(target, pred) # to compute Recall

precision = precision_score(target, pred) # to compute Precision

f1 = f1_score(target, pred) # to compute F1-score

# creating a dataframe of metrics

df_perf = pd.DataFrame(

{"Accuracy": acc, "Recall": recall, "Precision": precision, "F1": f1,},

index=[0],

)

return df_perf

In [42]:

def confusion_matrix_sklearn(model, predictors, target):

"""

To plot the confusion_matrix with percentages

model: classifier

predictors: independent variables

target: dependent variable

"""

y_pred = model.predict(predictors)

cm = confusion_matrix(target, y_pred)

labels = np.asarray(

[

["{0:0.0f}".format(item) + "\n{0:.2%}".format(item / cm.flatten().sum())]

for item in cm.flatten()

]

).reshape(2, 2)

plt.figure(figsize=(6, 4))

sns.heatmap(cm, annot=labels, fmt="")

plt.ylabel("True label")

plt.xlabel("Predicted label")

Build Decision Tree Model

In [43]:

model = DecisionTreeClassifier(criterion="gini", random_state=1) model.fit(X_train, y_train)

Out[43]:

DecisionTreeClassifier(random_state=1)

Checking model performance on training set

In [44]:

decision_tree_perf_train = model_performance_classification_sklearn(

model, X_train, y_train

)

decision_tree_perf_train

Out[44]:

| Accuracy | Recall | Precision | F1 | |

|---|---|---|---|---|

| 0 | 0.855514 | 0.9088 | 0.881563 | 0.894974 |

In [45]:

confusion_matrix_sklearn(model, X_train, y_train)

Checking model performance on test set

In [46]:

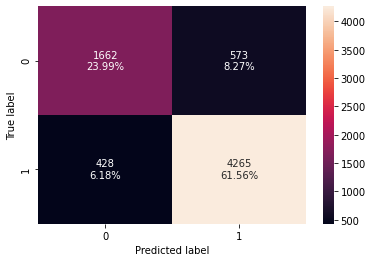

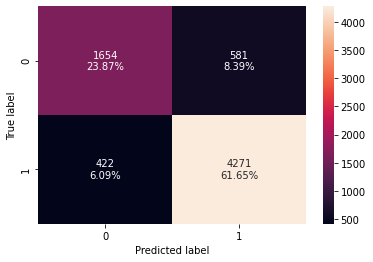

decision_tree_perf_test = model_performance_classification_sklearn(

model, X_test, y_test

)

decision_tree_perf_test

Out[46]:

| Accuracy | Recall | Precision | F1 | |

|---|---|---|---|---|

| 0 | 0.843723 | 0.897292 | 0.868606 | 0.882716 |

In [47]:

confusion_matrix_sklearn(model, X_test, y_test)

- Model is giving good and generalized results on training and test set.

Visualizing the Decision Tree

In [48]:

column_names = list(X.columns) feature_names = column_names print(feature_names)

['term_60 months', 'gender_Male', 'purpose_House', 'purpose_Medical', 'purpose_Other', 'purpose_Personal', 'purpose_Wedding', 'home_ownership_Own', 'home_ownership_Rent', 'age_>25', 'FICO_>500']

In [49]:

plt.figure(figsize=(20, 30))

out = tree.plot_tree(

model,

feature_names=feature_names,

filled=True,

fontsize=9,

node_ids=True,

class_names=True,

)

for o in out:

arrow = o.arrow_patch

if arrow is not None:

arrow.set_edgecolor("black")

arrow.set_linewidth(1)

plt.show()

In [50]:

# Text report showing the rules of a decision tree - print(tree.export_text(model, feature_names=feature_names, show_weights=True))

|--- FICO_>500 <= 0.50 | |--- term_60 months <= 0.50 | | |--- age_>25 <= 0.50 | | | |--- home_ownership_Rent <= 0.50 | | | | |--- purpose_Personal <= 0.50 | | | | | |--- gender_Male <= 0.50 | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | |--- purpose_Medical <= 0.50 | | | | | | | | |--- purpose_House <= 0.50 | | | | | | | | | |--- purpose_Other <= 0.50 | | | | | | | | | | |--- purpose_Wedding <= 0.50 | | | | | | | | | | | |--- weights: [1.00, 18.00] class: 1 | | | | | | | | | | |--- purpose_Wedding > 0.50 | | | | | | | | | | | |--- weights: [0.00, 9.00] class: 1 | | | | | | | | | |--- purpose_Other > 0.50 | | | | | | | | | | |--- weights: [0.00, 14.00] class: 1 | | | | | | | | |--- purpose_House > 0.50 | | | | | | | | | |--- weights: [7.00, 82.00] class: 1 | | | | | | | |--- purpose_Medical > 0.50 | | | | | | | | |--- weights: [1.00, 3.00] class: 1 | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | |--- purpose_Other <= 0.50 | | | | | | | | |--- purpose_House <= 0.50 | | | | | | | | | |--- weights: [2.00, 2.00] class: 0 | | | | | | | | |--- purpose_House > 0.50 | | | | | | | | | |--- weights: [4.00, 16.00] class: 1 | | | | | | | |--- purpose_Other > 0.50 | | | | | | | | |--- weights: [0.00, 2.00] class: 1 | | | | | |--- gender_Male > 0.50 | | | | | | |--- purpose_House <= 0.50 | | | | | | | |--- purpose_Other <= 0.50 | | | | | | | | |--- purpose_Medical <= 0.50 | | | | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | | | | |--- purpose_Wedding <= 0.50 | | | | | | | | | | | |--- weights: [30.00, 147.00] class: 1 | | | | | | | | | | |--- purpose_Wedding > 0.50 | | | | | | | | | | | |--- weights: [4.00, 15.00] class: 1 | | | | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | | | | |--- purpose_Wedding <= 0.50 | | | | | | | | | | | |--- weights: [8.00, 30.00] class: 1 | | | | | | | | | | |--- purpose_Wedding > 0.50 | | | | | | | | | | | |--- weights: [0.00, 4.00] class: 1 | | | | | | | | |--- purpose_Medical > 0.50 | | | | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | | | | |--- weights: [2.00, 13.00] class: 1 | | | | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | | | | |--- weights: [0.00, 2.00] class: 1 | | | | | | | |--- purpose_Other > 0.50 | | | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | | | |--- weights: [9.00, 51.00] class: 1 | | | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | | | |--- weights: [0.00, 18.00] class: 1 | | | | | | |--- purpose_House > 0.50 | | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | | |--- weights: [57.00, 438.00] class: 1 | | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | | |--- weights: [13.00, 70.00] class: 1 | | | | |--- purpose_Personal > 0.50 | | | | | |--- gender_Male <= 0.50 | | | | | | |--- weights: [0.00, 27.00] class: 1 | | | | | |--- gender_Male > 0.50 | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | |--- weights: [8.00, 91.00] class: 1 | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | |--- weights: [0.00, 13.00] class: 1 | | | |--- home_ownership_Rent > 0.50 | | | | |--- purpose_Personal <= 0.50 | | | | | |--- purpose_House <= 0.50 | | | | | | |--- purpose_Wedding <= 0.50 | | | | | | | |--- purpose_Other <= 0.50 | | | | | | | | |--- gender_Male <= 0.50 | | | | | | | | | |--- purpose_Medical <= 0.50 | | | | | | | | | | |--- weights: [5.00, 14.00] class: 1 | | | | | | | | | |--- purpose_Medical > 0.50 | | | | | | | | | | |--- weights: [0.00, 1.00] class: 1 | | | | | | | | |--- gender_Male > 0.50 | | | | | | | | | |--- purpose_Medical <= 0.50 | | | | | | | | | | |--- weights: [60.00, 201.00] class: 1 | | | | | | | | | |--- purpose_Medical > 0.50 | | | | | | | | | | |--- weights: [3.00, 10.00] class: 1 | | | | | | | |--- purpose_Other > 0.50 | | | | | | | | |--- gender_Male <= 0.50 | | | | | | | | | |--- weights: [2.00, 10.00] class: 1 | | | | | | | | |--- gender_Male > 0.50 | | | | | | | | | |--- weights: [9.00, 52.00] class: 1 | | | | | | |--- purpose_Wedding > 0.50 | | | | | | | |--- gender_Male <= 0.50 | | | | | | | | |--- weights: [0.00, 8.00] class: 1 | | | | | | | |--- gender_Male > 0.50 | | | | | | | | |--- weights: [5.00, 33.00] class: 1 | | | | | |--- purpose_House > 0.50 | | | | | | |--- gender_Male <= 0.50 | | | | | | | |--- weights: [14.00, 86.00] class: 1 | | | | | | |--- gender_Male > 0.50 | | | | | | | |--- weights: [114.00, 536.00] class: 1 | | | | |--- purpose_Personal > 0.50 | | | | | |--- weights: [0.00, 11.00] class: 1 | | |--- age_>25 > 0.50 | | | |--- weights: [0.00, 1291.00] class: 1 | |--- term_60 months > 0.50 | | |--- weights: [196.00, 0.00] class: 0 |--- FICO_>500 > 0.50 | |--- gender_Male <= 0.50 | | |--- age_>25 <= 0.50 | | | |--- purpose_Personal <= 0.50 | | | | |--- purpose_Wedding <= 0.50 | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | |--- purpose_Other <= 0.50 | | | | | | | |--- purpose_Medical <= 0.50 | | | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | | | |--- purpose_House <= 0.50 | | | | | | | | | | |--- weights: [31.00, 11.00] class: 0 | | | | | | | | | |--- purpose_House > 0.50 | | | | | | | | | | |--- weights: [120.00, 33.00] class: 0 | | | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | | | |--- purpose_House <= 0.50 | | | | | | | | | | |--- weights: [8.00, 1.00] class: 0 | | | | | | | | | |--- purpose_House > 0.50 | | | | | | | | | | |--- weights: [17.00, 7.00] class: 0 | | | | | | | |--- purpose_Medical > 0.50 | | | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | | | |--- weights: [4.00, 2.00] class: 0 | | | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | | | |--- weights: [1.00, 1.00] class: 0 | | | | | | |--- purpose_Other > 0.50 | | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | | |--- weights: [21.00, 4.00] class: 0 | | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | | |--- weights: [3.00, 0.00] class: 0 | | | | | |--- home_ownership_Rent > 0.50 | | | | | | |--- purpose_Medical <= 0.50 | | | | | | | |--- purpose_House <= 0.50 | | | | | | | | |--- purpose_Other <= 0.50 | | | | | | | | | |--- weights: [28.00, 9.00] class: 0 | | | | | | | | |--- purpose_Other > 0.50 | | | | | | | | | |--- weights: [13.00, 5.00] class: 0 | | | | | | | |--- purpose_House > 0.50 | | | | | | | | |--- weights: [120.00, 28.00] class: 0 | | | | | | |--- purpose_Medical > 0.50 | | | | | | | |--- weights: [4.00, 0.00] class: 0 | | | | |--- purpose_Wedding > 0.50 | | | | | |--- home_ownership_Own <= 0.50 | | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | | |--- weights: [6.00, 1.00] class: 0 | | | | | | |--- home_ownership_Rent > 0.50 | | | | | | | |--- weights: [9.00, 1.00] class: 0 | | | | | |--- home_ownership_Own > 0.50 | | | | | | |--- weights: [2.00, 1.00] class: 0 | | | |--- purpose_Personal > 0.50 | | | | |--- home_ownership_Rent <= 0.50 | | | | | |--- home_ownership_Own <= 0.50 | | | | | | |--- weights: [37.00, 6.00] class: 0 | | | | | |--- home_ownership_Own > 0.50 | | | | | | |--- weights: [1.00, 0.00] class: 0 | | | | |--- home_ownership_Rent > 0.50 | | | | | |--- weights: [3.00, 0.00] class: 0 | | |--- age_>25 > 0.50 | | | |--- purpose_Other <= 0.50 | | | | |--- purpose_Personal <= 0.50 | | | | | |--- purpose_House <= 0.50 | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | |--- purpose_Medical <= 0.50 | | | | | | | | |--- purpose_Wedding <= 0.50 | | | | | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | | | | | |--- weights: [49.00, 12.00] class: 0 | | | | | | | | | |--- home_ownership_Rent > 0.50 | | | | | | | | | | |--- weights: [53.00, 16.00] class: 0 | | | | | | | | |--- purpose_Wedding > 0.50 | | | | | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | | | | | |--- weights: [10.00, 3.00] class: 0 | | | | | | | | | |--- home_ownership_Rent > 0.50 | | | | | | | | | | |--- weights: [17.00, 3.00] class: 0 | | | | | | | |--- purpose_Medical > 0.50 | | | | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | | | | |--- weights: [6.00, 1.00] class: 0 | | | | | | | | |--- home_ownership_Rent > 0.50 | | | | | | | | | |--- weights: [6.00, 1.00] class: 0 | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | |--- weights: [3.00, 0.00] class: 0 | | | | | |--- purpose_House > 0.50 | | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | | |--- weights: [170.00, 48.00] class: 0 | | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | | |--- weights: [29.00, 10.00] class: 0 | | | | | | |--- home_ownership_Rent > 0.50 | | | | | | | |--- weights: [168.00, 54.00] class: 0 | | | | |--- purpose_Personal > 0.50 | | | | | |--- home_ownership_Own <= 0.50 | | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | | |--- weights: [44.00, 21.00] class: 0 | | | | | | |--- home_ownership_Rent > 0.50 | | | | | | | |--- weights: [1.00, 1.00] class: 0 | | | | | |--- home_ownership_Own > 0.50 | | | | | | |--- weights: [5.00, 1.00] class: 0 | | | |--- purpose_Other > 0.50 | | | | |--- home_ownership_Own <= 0.50 | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | |--- weights: [31.00, 15.00] class: 0 | | | | | |--- home_ownership_Rent > 0.50 | | | | | | |--- weights: [24.00, 13.00] class: 0 | | | | |--- home_ownership_Own > 0.50 | | | | | |--- weights: [4.00, 1.00] class: 0 | |--- gender_Male > 0.50 | | |--- age_>25 <= 0.50 | | | |--- term_60 months <= 0.50 | | | | |--- home_ownership_Rent <= 0.50 | | | | | |--- home_ownership_Own <= 0.50 | | | | | | |--- purpose_Medical <= 0.50 | | | | | | | |--- purpose_Personal <= 0.50 | | | | | | | | |--- purpose_Other <= 0.50 | | | | | | | | | |--- purpose_Wedding <= 0.50 | | | | | | | | | | |--- purpose_House <= 0.50 | | | | | | | | | | | |--- weights: [21.00, 7.00] class: 0 | | | | | | | | | | |--- purpose_House > 0.50 | | | | | | | | | | | |--- weights: [96.00, 33.00] class: 0 | | | | | | | | | |--- purpose_Wedding > 0.50 | | | | | | | | | | |--- weights: [2.00, 1.00] class: 0 | | | | | | | | |--- purpose_Other > 0.50 | | | | | | | | | |--- weights: [18.00, 5.00] class: 0 | | | | | | | |--- purpose_Personal > 0.50 | | | | | | | | |--- weights: [17.00, 3.00] class: 0 | | | | | | |--- purpose_Medical > 0.50 | | | | | | | |--- weights: [2.00, 2.00] class: 0 | | | | | |--- home_ownership_Own > 0.50 | | | | | | |--- purpose_House <= 0.50 | | | | | | | |--- purpose_Wedding <= 0.50 | | | | | | | | |--- purpose_Personal <= 0.50 | | | | | | | | | |--- purpose_Other <= 0.50 | | | | | | | | | | |--- weights: [1.00, 4.00] class: 1 | | | | | | | | | |--- purpose_Other > 0.50 | | | | | | | | | | |--- weights: [2.00, 2.00] class: 0 | | | | | | | | |--- purpose_Personal > 0.50 | | | | | | | | | |--- weights: [1.00, 0.00] class: 0 | | | | | | | |--- purpose_Wedding > 0.50 | | | | | | | | |--- weights: [1.00, 0.00] class: 0 | | | | | | |--- purpose_House > 0.50 | | | | | | | |--- weights: [12.00, 5.00] class: 0 | | | | |--- home_ownership_Rent > 0.50 | | | | | |--- purpose_Wedding <= 0.50 | | | | | | |--- purpose_Other <= 0.50 | | | | | | | |--- purpose_House <= 0.50 | | | | | | | | |--- purpose_Medical <= 0.50 | | | | | | | | | |--- weights: [14.00, 8.00] class: 0 | | | | | | | | |--- purpose_Medical > 0.50 | | | | | | | | | |--- weights: [2.00, 1.00] class: 0 | | | | | | | |--- purpose_House > 0.50 | | | | | | | | |--- weights: [71.00, 38.00] class: 0 | | | | | | |--- purpose_Other > 0.50 | | | | | | | |--- weights: [8.00, 6.00] class: 0 | | | | | |--- purpose_Wedding > 0.50 | | | | | | |--- weights: [9.00, 3.00] class: 0 | | | |--- term_60 months > 0.50 | | | | |--- purpose_House <= 0.50 | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | |--- purpose_Personal <= 0.50 | | | | | | | | |--- purpose_Medical <= 0.50 | | | | | | | | | |--- purpose_Wedding <= 0.50 | | | | | | | | | | |--- purpose_Other <= 0.50 | | | | | | | | | | | |--- weights: [1.00, 13.00] class: 1 | | | | | | | | | | |--- purpose_Other > 0.50 | | | | | | | | | | | |--- weights: [0.00, 2.00] class: 1 | | | | | | | | | |--- purpose_Wedding > 0.50 | | | | | | | | | | |--- weights: [0.00, 2.00] class: 1 | | | | | | | | |--- purpose_Medical > 0.50 | | | | | | | | | |--- weights: [1.00, 9.00] class: 1 | | | | | | | |--- purpose_Personal > 0.50 | | | | | | | | |--- weights: [1.00, 7.00] class: 1 | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | |--- weights: [0.00, 7.00] class: 1 | | | | | |--- home_ownership_Rent > 0.50 | | | | | | |--- purpose_Personal <= 0.50 | | | | | | | |--- purpose_Medical <= 0.50 | | | | | | | | |--- purpose_Other <= 0.50 | | | | | | | | | |--- purpose_Wedding <= 0.50 | | | | | | | | | | |--- weights: [2.00, 14.00] class: 1 | | | | | | | | | |--- purpose_Wedding > 0.50 | | | | | | | | | | |--- weights: [0.00, 1.00] class: 1 | | | | | | | | |--- purpose_Other > 0.50 | | | | | | | | | |--- weights: [2.00, 8.00] class: 1 | | | | | | | |--- purpose_Medical > 0.50 | | | | | | | | |--- weights: [1.00, 3.00] class: 1 | | | | | | |--- purpose_Personal > 0.50 | | | | | | | |--- weights: [2.00, 4.00] class: 1 | | | | |--- purpose_House > 0.50 | | | | | |--- home_ownership_Own <= 0.50 | | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | | |--- weights: [14.00, 53.00] class: 1 | | | | | | |--- home_ownership_Rent > 0.50 | | | | | | | |--- weights: [10.00, 41.00] class: 1 | | | | | |--- home_ownership_Own > 0.50 | | | | | | |--- weights: [2.00, 12.00] class: 1 | | |--- age_>25 > 0.50 | | | |--- term_60 months <= 0.50 | | | | |--- purpose_Medical <= 0.50 | | | | | |--- purpose_Wedding <= 0.50 | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | |--- purpose_House <= 0.50 | | | | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | | | | |--- purpose_Personal <= 0.50 | | | | | | | | | | |--- purpose_Other <= 0.50 | | | | | | | | | | | |--- weights: [19.00, 67.00] class: 1 | | | | | | | | | | |--- purpose_Other > 0.50 | | | | | | | | | | | |--- weights: [5.00, 29.00] class: 1 | | | | | | | | | |--- purpose_Personal > 0.50 | | | | | | | | | | |--- weights: [9.00, 48.00] class: 1 | | | | | | | | |--- home_ownership_Rent > 0.50 | | | | | | | | | |--- purpose_Personal <= 0.50 | | | | | | | | | | |--- purpose_Other <= 0.50 | | | | | | | | | | | |--- weights: [11.00, 64.00] class: 1 | | | | | | | | | | |--- purpose_Other > 0.50 | | | | | | | | | | | |--- weights: [7.00, 33.00] class: 1 | | | | | | | | | |--- purpose_Personal > 0.50 | | | | | | | | | | |--- weights: [1.00, 3.00] class: 1 | | | | | | | |--- purpose_House > 0.50 | | | | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | | | | |--- weights: [53.00, 219.00] class: 1 | | | | | | | | |--- home_ownership_Rent > 0.50 | | | | | | | | | |--- weights: [51.00, 206.00] class: 1 | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | |--- purpose_Other <= 0.50 | | | | | | | | |--- purpose_Personal <= 0.50 | | | | | | | | | |--- purpose_House <= 0.50 | | | | | | | | | | |--- weights: [0.00, 15.00] class: 1 | | | | | | | | | |--- purpose_House > 0.50 | | | | | | | | | | |--- weights: [5.00, 38.00] class: 1 | | | | | | | | |--- purpose_Personal > 0.50 | | | | | | | | | |--- weights: [2.00, 4.00] class: 1 | | | | | | | |--- purpose_Other > 0.50 | | | | | | | | |--- weights: [2.00, 3.00] class: 1 | | | | | |--- purpose_Wedding > 0.50 | | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | | |--- home_ownership_Own <= 0.50 | | | | | | | | |--- weights: [0.00, 9.00] class: 1 | | | | | | | |--- home_ownership_Own > 0.50 | | | | | | | | |--- weights: [2.00, 2.00] class: 0 | | | | | | |--- home_ownership_Rent > 0.50 | | | | | | | |--- weights: [7.00, 14.00] class: 1 | | | | |--- purpose_Medical > 0.50 | | | | | |--- home_ownership_Rent <= 0.50 | | | | | | |--- weights: [4.00, 9.00] class: 1 | | | | | |--- home_ownership_Rent > 0.50 | | | | | | |--- weights: [4.00, 8.00] class: 1 | | | |--- term_60 months > 0.50 | | | | |--- weights: [138.00, 0.00] class: 0

In [51]:

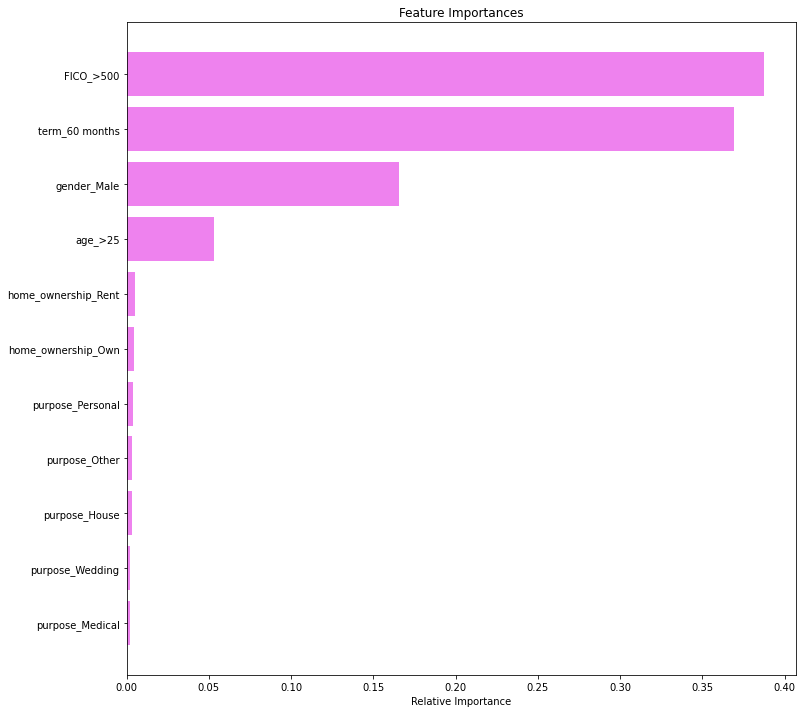

importances = model.feature_importances_

indices = np.argsort(importances)

plt.figure(figsize=(12, 12))

plt.title("Feature Importances")

plt.barh(range(len(indices)), importances[indices], color="violet", align="center")

plt.yticks(range(len(indices)), [feature_names[i] for i in indices])

plt.xlabel("Relative Importance")

plt.show()

- FICO score, duration of loan and gender are the top 3 important features.

Using GridSearch for Hyperparameter tuning of our tree model

- Let’s see if we can improve our model performance even more.

In [52]:

# Choose the type of classifier.

estimator = DecisionTreeClassifier(random_state=1)

# Grid of parameters to choose from

parameters = {

"max_depth": [np.arange(2, 50, 5), None],

"criterion": ["entropy", "gini"],

"splitter": ["best", "random"],

"min_impurity_decrease": [0.000001, 0.00001, 0.0001],

}

# Type of scoring used to compare parameter combinations

acc_scorer = make_scorer(recall_score)

# Run the grid search

grid_obj = GridSearchCV(estimator, parameters, scoring=acc_scorer, cv=5)

grid_obj = grid_obj.fit(X_train, y_train)

# Set the clf to the best combination of parameters

estimator = grid_obj.best_estimator_

# Fit the best algorithm to the data.

estimator.fit(X_train, y_train)

Out[52]:

DecisionTreeClassifier(min_impurity_decrease=0.0001, random_state=1)

Checking performance on training set

In [53]:

decision_tree_tune_perf_train = model_performance_classification_sklearn(

estimator, X_train, y_train

)

decision_tree_tune_perf_train

Out[53]:

| Accuracy | Recall | Precision | F1 | |

|---|---|---|---|---|

| 0 | 0.855225 | 0.910079 | 0.880256 | 0.894919 |

In [54]:

confusion_matrix_sklearn(estimator, X_train, y_train)

- The Recall has improved on the training set as compared to the initial model.

Checking model performance on test set

In [55]:

decision_tree_tune_perf_test = model_performance_classification_sklearn(

estimator, X_test, y_test

)

decision_tree_tune_perf_test

Out[55]:

| Accuracy | Recall | Precision | F1 | |

|---|---|---|---|---|

| 0 | 0.843939 | 0.898613 | 0.867943 | 0.883012 |

In [56]:

confusion_matrix_sklearn(estimator, X_test, y_test)

- After hyperparameter tuning the model has performance has remained same and the model has become simpler.

In [57]:

plt.figure(figsize=(15, 12))

tree.plot_tree(

estimator,

feature_names=feature_names,

filled=True,

fontsize=9,

node_ids=True,

class_names=True,

)

plt.show()

- We are getting a simplified tree after pre-pruning.

Cost Complexity Pruning

In [58]:

clf = DecisionTreeClassifier(random_state=1) path = clf.cost_complexity_pruning_path(X_train, y_train) ccp_alphas, impurities = path.ccp_alphas, path.impurities

In [59]:

pd.DataFrame(path)

Out[59]:

| ccp_alphas | impurities | |

|---|---|---|

| 0 | 0.000000e+00 | 0.226403 |

| 1 | 0.000000e+00 | 0.226403 |

| 2 | 2.794668e-09 | 0.226403 |

| 3 | 2.244984e-07 | 0.226403 |

| 4 | 4.918264e-07 | 0.226404 |

| 5 | 6.998390e-07 | 0.226404 |

| 6 | 7.597561e-07 | 0.226405 |

| 7 | 1.058874e-06 | 0.226406 |

| 8 | 1.184343e-06 | 0.226407 |

| 9 | 1.386119e-06 | 0.226409 |

| 10 | 2.183321e-06 | 0.226411 |

| 11 | 2.291140e-06 | 0.226416 |

| 12 | 3.665824e-06 | 0.226419 |

| 13 | 3.778517e-06 | 0.226423 |

| 14 | 4.160227e-06 | 0.226431 |

| 15 | 4.169086e-06 | 0.226435 |

| 16 | 4.245347e-06 | 0.226440 |

| 17 | 5.155064e-06 | 0.226445 |

| 18 | 5.244266e-06 | 0.226450 |

| 19 | 5.492923e-06 | 0.226456 |

| 20 | 6.045620e-06 | 0.226462 |

| 21 | 8.340601e-06 | 0.226470 |

| 22 | 8.765875e-06 | 0.226479 |

| 23 | 9.056740e-06 | 0.226488 |

| 24 | 9.751114e-06 | 0.226498 |

| 25 | 1.058022e-05 | 0.226519 |

| 26 | 1.138027e-05 | 0.226542 |

| 27 | 1.155642e-05 | 0.226553 |

| 28 | 1.156951e-05 | 0.226576 |

| 29 | 1.169925e-05 | 0.226600 |

| 30 | 1.174875e-05 | 0.226611 |

| 31 | 1.202848e-05 | 0.226623 |

| 32 | 1.323848e-05 | 0.226637 |

| 33 | 1.507632e-05 | 0.226652 |

| 34 | 1.608110e-05 | 0.226668 |

| 35 | 1.753314e-05 | 0.226685 |

| 36 | 1.979545e-05 | 0.226705 |

| 37 | 2.032168e-05 | 0.226725 |

| 38 | 2.166168e-05 | 0.226747 |

| 39 | 2.168081e-05 | 0.226812 |

| 40 | 2.216324e-05 | 0.226834 |

| 41 | 2.421893e-05 | 0.226931 |

| 42 | 2.477532e-05 | 0.226956 |

| 43 | 2.568272e-05 | 0.226982 |

| 44 | 3.132587e-05 | 0.227013 |

| 45 | 3.194772e-05 | 0.227077 |

| 46 | 3.204299e-05 | 0.227109 |

| 47 | 3.303016e-05 | 0.227142 |

| 48 | 3.424580e-05 | 0.227176 |

| 49 | 3.522919e-05 | 0.227211 |

| 50 | 3.529801e-05 | 0.227247 |

| 51 | 3.745085e-05 | 0.227284 |

| 52 | 3.999700e-05 | 0.227324 |

| 53 | 4.034344e-05 | 0.227566 |

| 54 | 4.156233e-05 | 0.227608 |

| 55 | 4.295438e-05 | 0.227651 |

| 56 | 4.320199e-05 | 0.227694 |

| 57 | 4.340672e-05 | 0.227737 |

| 58 | 5.348017e-05 | 0.227791 |

| 59 | 5.773672e-05 | 0.227849 |

| 60 | 5.995736e-05 | 0.227968 |

| 61 | 7.314108e-05 | 0.228115 |

| 62 | 7.574157e-05 | 0.228190 |

| 63 | 7.818003e-05 | 0.228347 |

| 64 | 8.769179e-05 | 0.228435 |

| 65 | 8.831375e-05 | 0.228523 |

| 66 | 9.072968e-05 | 0.228795 |

| 67 | 1.049759e-04 | 0.229005 |

| 68 | 1.076388e-04 | 0.229436 |

| 69 | 1.117546e-04 | 0.229771 |

| 70 | 1.193296e-04 | 0.230009 |

| 71 | 1.217918e-04 | 0.230131 |

| 72 | 1.233812e-04 | 0.230255 |

| 73 | 1.527711e-04 | 0.230407 |

| 74 | 1.553389e-04 | 0.230563 |

| 75 | 1.773114e-04 | 0.230917 |

| 76 | 1.799582e-04 | 0.231097 |

| 77 | 2.040456e-04 | 0.231301 |

| 78 | 6.198757e-04 | 0.231921 |

| 79 | 5.448168e-03 | 0.237369 |

| 80 | 1.124860e-02 | 0.248618 |

| 81 | 1.417137e-02 | 0.276961 |

| 82 | 3.466595e-02 | 0.311627 |

| 83 | 4.376431e-02 | 0.355391 |

| 84 | 8.167025e-02 | 0.437061 |

In [60]:

fig, ax = plt.subplots(figsize=(15, 5))

ax.plot(ccp_alphas[:-1], impurities[:-1], marker="o", drawstyle="steps-post")

ax.set_xlabel("effective alpha")

ax.set_ylabel("total impurity of leaves")

ax.set_title("Total Impurity vs effective alpha for training set")

plt.show()

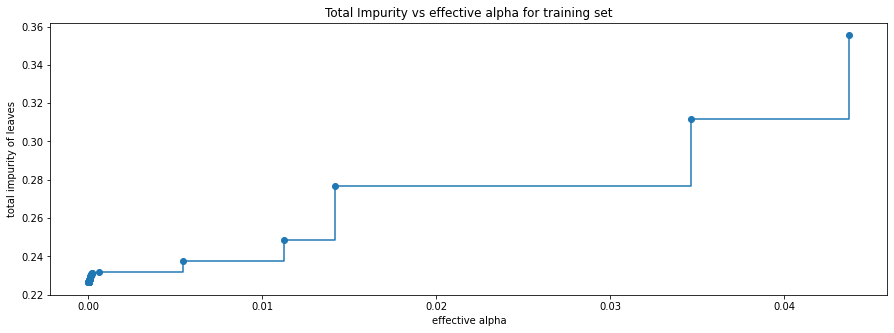

Next, we train a decision tree using the effective alphas. The last value in ccp_alphas is the alpha value that prunes the whole tree, leaving the tree, clfs[-1], with one node.

In [61]:

clfs = []

for ccp_alpha in ccp_alphas:

clf = DecisionTreeClassifier(random_state=1, ccp_alpha=ccp_alpha)

clf.fit(X_train, y_train)

clfs.append(clf)

print(

"Number of nodes in the last tree is: {} with ccp_alpha: {}".format(

clfs[-1].tree_.node_count, ccp_alphas[-1]

)

)

Number of nodes in the last tree is: 1 with ccp_alpha: 0.08167024657332106

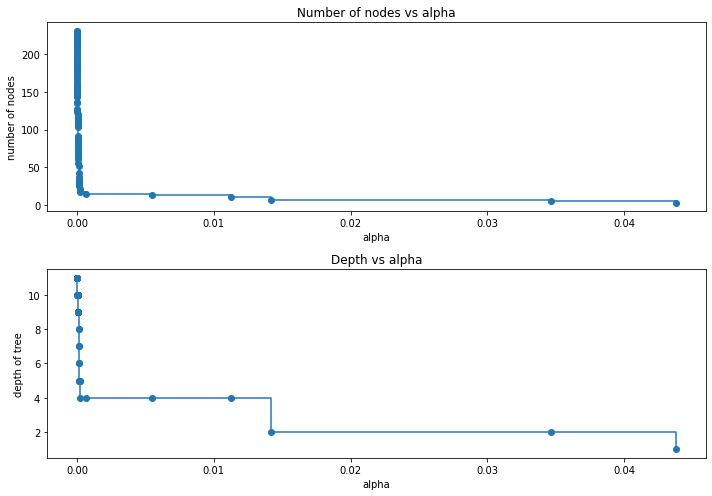

For the remainder, we remove the last element in clfs and ccp_alphas, because it is the trivial tree with only one node. Here we show that the number of nodes and tree depth decreases as alpha increases.

In [62]:

clfs = clfs[:-1]

ccp_alphas = ccp_alphas[:-1]

node_counts = [clf.tree_.node_count for clf in clfs]

depth = [clf.tree_.max_depth for clf in clfs]

fig, ax = plt.subplots(2, 1, figsize=(10, 7))

ax[0].plot(ccp_alphas, node_counts, marker="o", drawstyle="steps-post")

ax[0].set_xlabel("alpha")

ax[0].set_ylabel("number of nodes")

ax[0].set_title("Number of nodes vs alpha")

ax[1].plot(ccp_alphas, depth, marker="o", drawstyle="steps-post")

ax[1].set_xlabel("alpha")

ax[1].set_ylabel("depth of tree")

ax[1].set_title("Depth vs alpha")

fig.tight_layout()

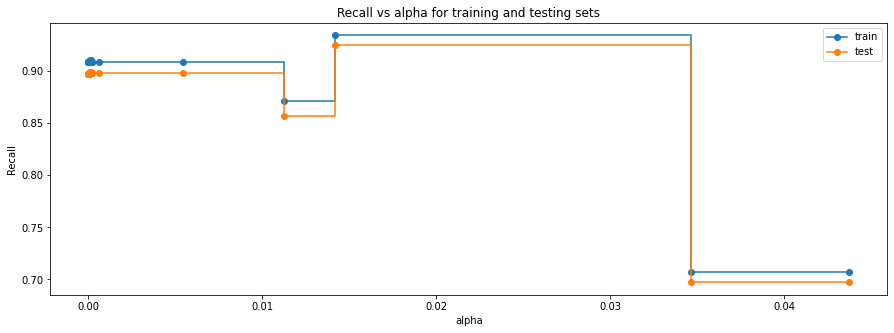

Recall vs alpha for training and testing sets

In [63]:

recall_train = []

for clf in clfs:

pred_train = clf.predict(X_train)

values_train = recall_score(y_train, pred_train)

recall_train.append(values_train)

In [64]:

recall_test = []

for clf in clfs:

pred_test = clf.predict(X_test)

values_test = recall_score(y_test, pred_test)

recall_test.append(values_test)

In [65]:

fig, ax = plt.subplots(figsize=(15, 5))

ax.set_xlabel("alpha")

ax.set_ylabel("Recall")

ax.set_title("Recall vs alpha for training and testing sets")

ax.plot(ccp_alphas, recall_train, marker="o", label="train", drawstyle="steps-post")

ax.plot(ccp_alphas, recall_test, marker="o", label="test", drawstyle="steps-post")

ax.legend()

plt.show()

In [66]:

# creating the model where we get highest train and test recall index_best_model = np.argmax(recall_test) best_model = clfs[index_best_model] print(best_model)

DecisionTreeClassifier(ccp_alpha=0.014171370928955346, random_state=1)

Checking model performance on training set

In [67]:

decision_tree_postpruned_perf_train = model_performance_classification_sklearn(

best_model, X_train, y_train

)

decision_tree_postpruned_perf_train

Out[67]:

| Accuracy | Recall | Precision | F1 | |

|---|---|---|---|---|

| 0 | 0.812211 | 0.933944 | 0.815594 | 0.870766 |

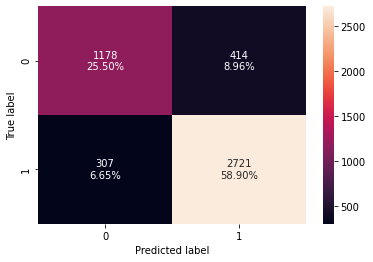

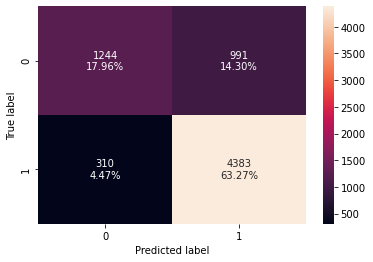

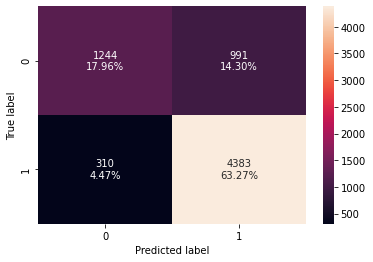

In [68]:

confusion_matrix_sklearn(best_model, X_train, y_train)

Checking model performance on test set

In [69]:

decision_tree_postpruned_perf_test = model_performance_classification_sklearn(

best_model, X_test, y_test

)

decision_tree_postpruned_perf_test

Out[69]:

| Accuracy | Recall | Precision | F1 | |

|---|---|---|---|---|

| 0 | 0.798052 | 0.924703 | 0.798859 | 0.857187 |

In [70]:

confusion_matrix_sklearn(best_model, X_train, y_train)

- With post-pruning we are getting good and generalized model performance on both training and test set.

- The recall has improved further.

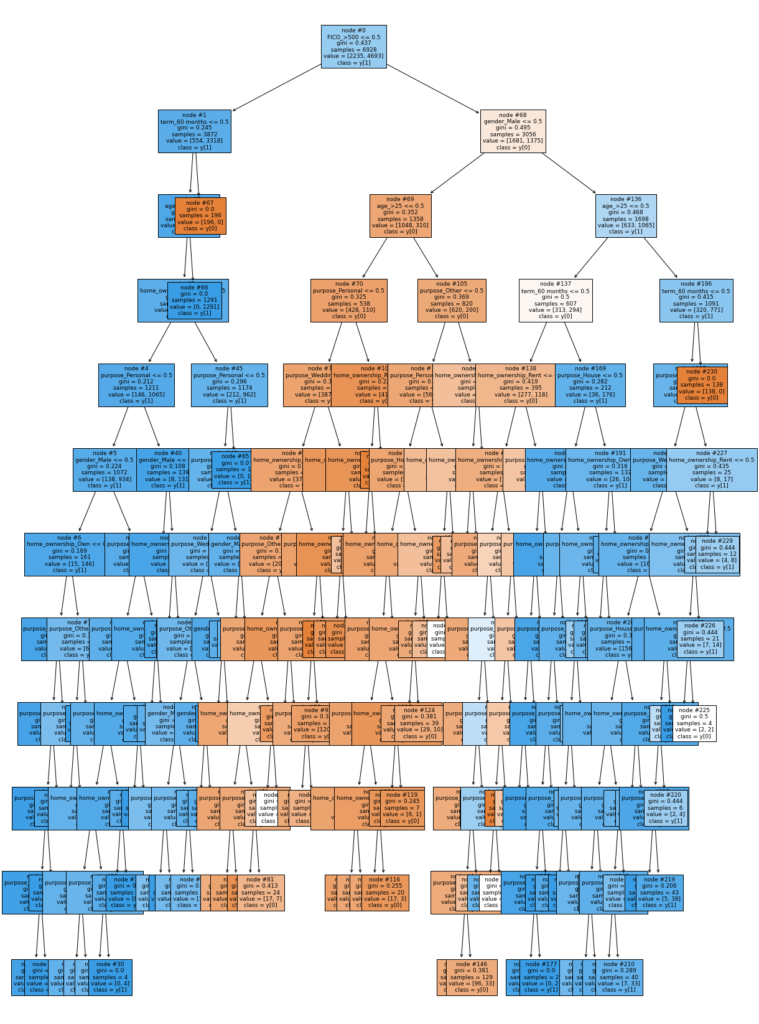

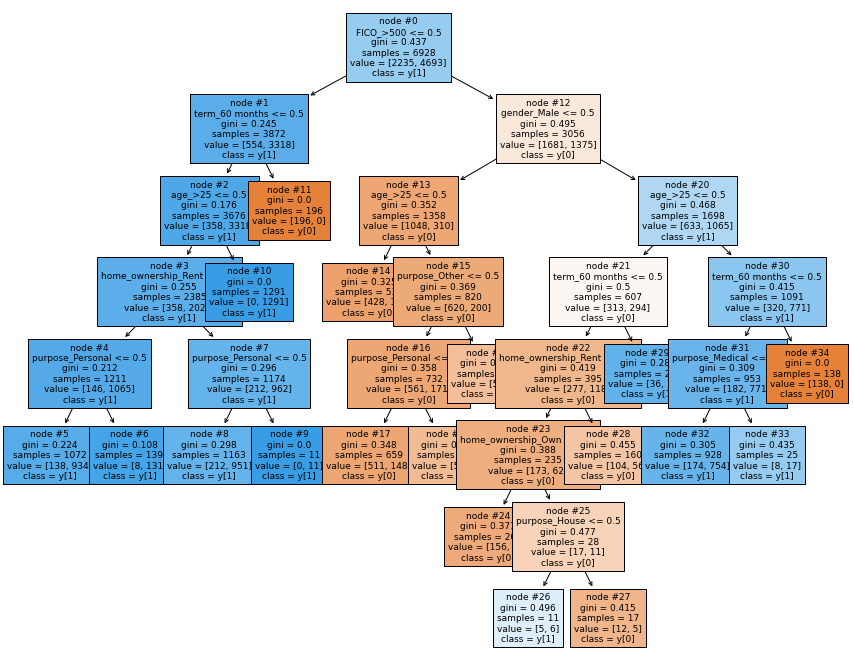

Visualizing the Decision Tree

In [71]:

plt.figure(figsize=(10, 10))

out = tree.plot_tree(

best_model,

feature_names=feature_names,

filled=True,

fontsize=9,

node_ids=True,

class_names=True,

)

for o in out:

arrow = o.arrow_patch

if arrow is not None:

arrow.set_edgecolor("black")

arrow.set_linewidth(1)

plt.show()

plt.show()

In [72]:

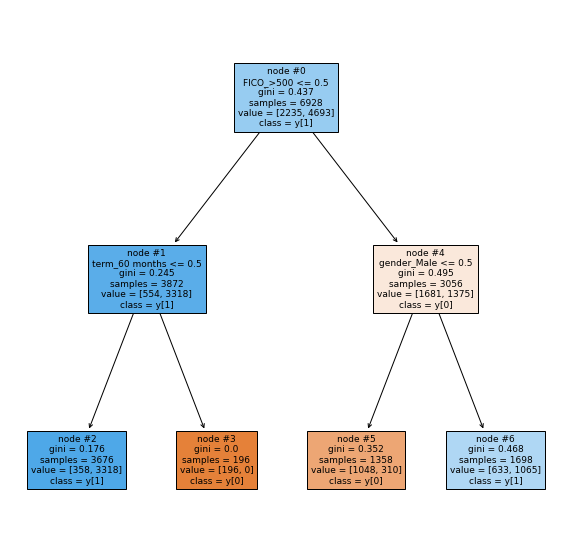

# Text report showing the rules of a decision tree - print(tree.export_text(best_model, feature_names=feature_names, show_weights=True))

|--- FICO_>500 <= 0.50 | |--- term_60 months <= 0.50 | | |--- weights: [358.00, 3318.00] class: 1 | |--- term_60 months > 0.50 | | |--- weights: [196.00, 0.00] class: 0 |--- FICO_>500 > 0.50 | |--- gender_Male <= 0.50 | | |--- weights: [1048.00, 310.00] class: 0 | |--- gender_Male > 0.50 | | |--- weights: [633.00, 1065.00] class: 1

In [73]:

# importance of features in the tree building ( The importance of a feature is computed as the

# (normalized) total reduction of the 'criterion' brought by that feature. It is also known as the Gini importance )

print(

pd.DataFrame(

best_model.feature_importances_, columns=["Imp"], index=X_train.columns

).sort_values(by="Imp", ascending=False)

)

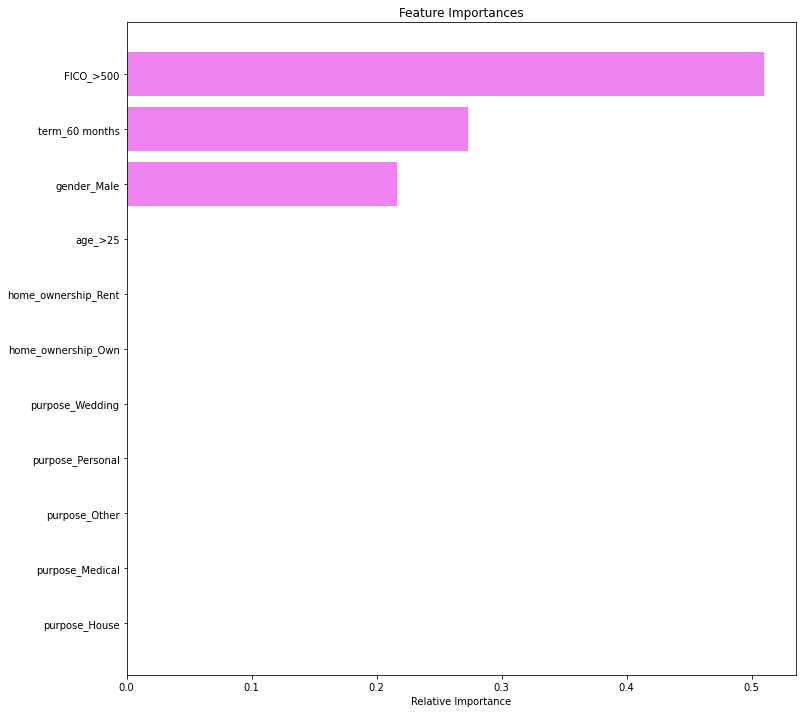

Imp FICO_>500 0.510119 term_60 months 0.273355 gender_Male 0.216526 purpose_House 0.000000 purpose_Medical 0.000000 purpose_Other 0.000000 purpose_Personal 0.000000 purpose_Wedding 0.000000 home_ownership_Own 0.000000 home_ownership_Rent 0.000000 age_>25 0.000000

In [74]:

importances = best_model.feature_importances_

indices = np.argsort(importances)

plt.figure(figsize=(12, 12))

plt.title("Feature Importances")

plt.barh(range(len(indices)), importances[indices], color="violet", align="center")

plt.yticks(range(len(indices)), [feature_names[i] for i in indices])

plt.xlabel("Relative Importance")

plt.show()

- FICO score, duration of the loan, and gender remain the most important feature with post-pruning too.

Comparing all the decision tree models

In [75]:

# training performance comparison

models_train_comp_df = pd.concat(

[

decision_tree_perf_train.T,

decision_tree_tune_perf_train.T,

decision_tree_postpruned_perf_train.T,

],

axis=1,

)

models_train_comp_df.columns = [

"Decision Tree sklearn",

"Decision Tree (Pre-Pruning)",

"Decision Tree (Post-Pruning)",

]

print("Training performance comparison:")

models_train_comp_df

Training performance comparison:

Out[75]:

| Decision Tree sklearn | Decision Tree (Pre-Pruning) | Decision Tree (Post-Pruning) | |

|---|---|---|---|

| Accuracy | 0.855514 | 0.855225 | 0.812211 |

| Recall | 0.908800 | 0.910079 | 0.933944 |

| Precision | 0.881563 | 0.880256 | 0.815594 |

| F1 | 0.894974 | 0.894919 | 0.870766 |

In [76]:

# test performance comparison

models_train_comp_df = pd.concat(

[

decision_tree_perf_test.T,

decision_tree_tune_perf_test.T,

decision_tree_postpruned_perf_test.T,

],

axis=1,

)

models_train_comp_df.columns = [

"Decision Tree sklearn",

"Decision Tree (Pre-Pruning)",

"Decision Tree (Post-Pruning)",

]

print("Test set performance comparison:")

models_train_comp_df

Test set performance comparison:

Out[76]:

| Decision Tree sklearn | Decision Tree (Pre-Pruning) | Decision Tree (Post-Pruning) | |

|---|---|---|---|

| Accuracy | 0.843723 | 0.843939 | 0.798052 |

| Recall | 0.897292 | 0.898613 | 0.924703 |

| Precision | 0.868606 | 0.867943 | 0.798859 |

| F1 | 0.882716 | 0.883012 | 0.857187 |

- Decision tree with post-pruning is giving the highest recall on the test set.

- The tree with post pruning is not complex and easy to interpret.

Business Insights

- FICO, term and gender (in that order) are the most important variables in determining if a borrower will get into a delinquent stage

- No borrower shall be given a loan if they are applying for a 36 month term loan and have a FICO score in the range 300-500.

- Female borrowers with a FICO score greater than 500 should be our target customers.

- Criteria to approve loan according to decision tree model should depend on three main factors – FICO score, duration of loan and gender that is – If the FICO score is less than 500 and the duration of loan is less than 60 months then the customer will not be able to repay the loans. If the customer has greater than 500 FICO score and is a female higher chances that they will repay the loans.